rewrite this content and keep HTML tags as is. This is content from rss feed and I don’t need their *Daily Debrief Newsletter*, their tags from bottom like this *Share this articleCategoriesTags*, Editorial Process section, phrases like *Featured image from Peakpx, chart from Tradingview.com*, SPECIAL OFFERS and similar sections – just remove such sections and save only article itself:

Cryptocurrency exchange OKX has rolled out the beta launch of its marketplace for artificial intelligence (AI) agents.

The OKX AI platform enables users to list their own AI agents, enables AI agents to find work, transact autonomously and build an onchain reputation, according to a Tuesday announcement shared with Cointelegraph.

The platform connects two marketplaces: An agent marketplace where builders can earn income by listing their AI agents for services and a task marketplace where agents post work and find other agents for their tasks.

Agentic AI is expected to drive a 24-fold increase in token consumption, that is units of compute, by 2030 as consumers and enterprises adopt the technology, Goldman Sachs Research said last month. OKX is the latest crypto platform to venture into AI infrastructure, following similar initiatives from Coinbase, MetaMask and Nansen.

The marketplace will remain in beta until “consistent, repeat usage patterns” emerge among users, with trading, onchain activity and research tasks expected to become the primary early categories on the platform, a spokesperson for OKX told Cointelegraph.

“OKX is economic infrastructure for agentic commerce. Nobody is combining identity, reputation, payments, and a skills marketplace into one platform,” explained the spokesperson.

OKX AI agent marketplace. Source: OKX.ai

AI agent builds will be paid in Stablecoins, initially Tether’s USDT (USDT) and Paxos’ Global Dollar (USDG). Payments will settle through escrow-based contracts for complex work or instant pay-per-call transactions for standardized services.

Disputes will be resolved by a staked network of evaluators, instead of a central entity. All types of tasks will contribute to the same onchain reputation of AI agents, which is managed through the OKX Agentic Wallet.

The marketplace launches with support from companies including Amazon Web Services (AWS), AltLayer, CertiK, the Ethereum Foundation, the Solana Foundation, Opentensor Foundation and StraitsX.

Onchain reputation seeks to prevent malicious AI agents

The onchain reputation and escrow system is built to create trust in AI agents by tracking their work history. Agents with no track record or a history of failed or disputed work will be less likely to get hired by other agents.

For larger projects, payment sits in escrow until the task is completed and verified, which aims to “limit” the damage a bad actor can cause in a single transaction.

A spokesperson for OKX said that the onchain reputation system will prevent agents from hiring other malicious agents, especially as more transaction history accumulates.

The spokesperson said the platform is working on additional defense layers, including more sophisticated dispute resolution and an anomaly detection system against coordinated bad-actor behavior.

Crypto platforms join AI wave as agentic payments increase

Cryptocurrency platforms are venturing into autonomous AI infrastructure. On June 12, Coinbase launched a tool that allows AI agents to make payments and trade crypto on behalf of users.

Days earlier, MetaMask launched a self-custodial cryptocurrency wallet that enables AI agents to transact across decentralized finance protocols within user-defined spending and security limits, as reported by Cointelegraph on June 8.

In January, crypto analytics platform Nansen launched autonomous cryptocurrency trading tools that enabled users to execute trades through natural language prompts, instead of traditional charts or order books.

Related: Not every AI agent needs its own cryptocurrency: CZ

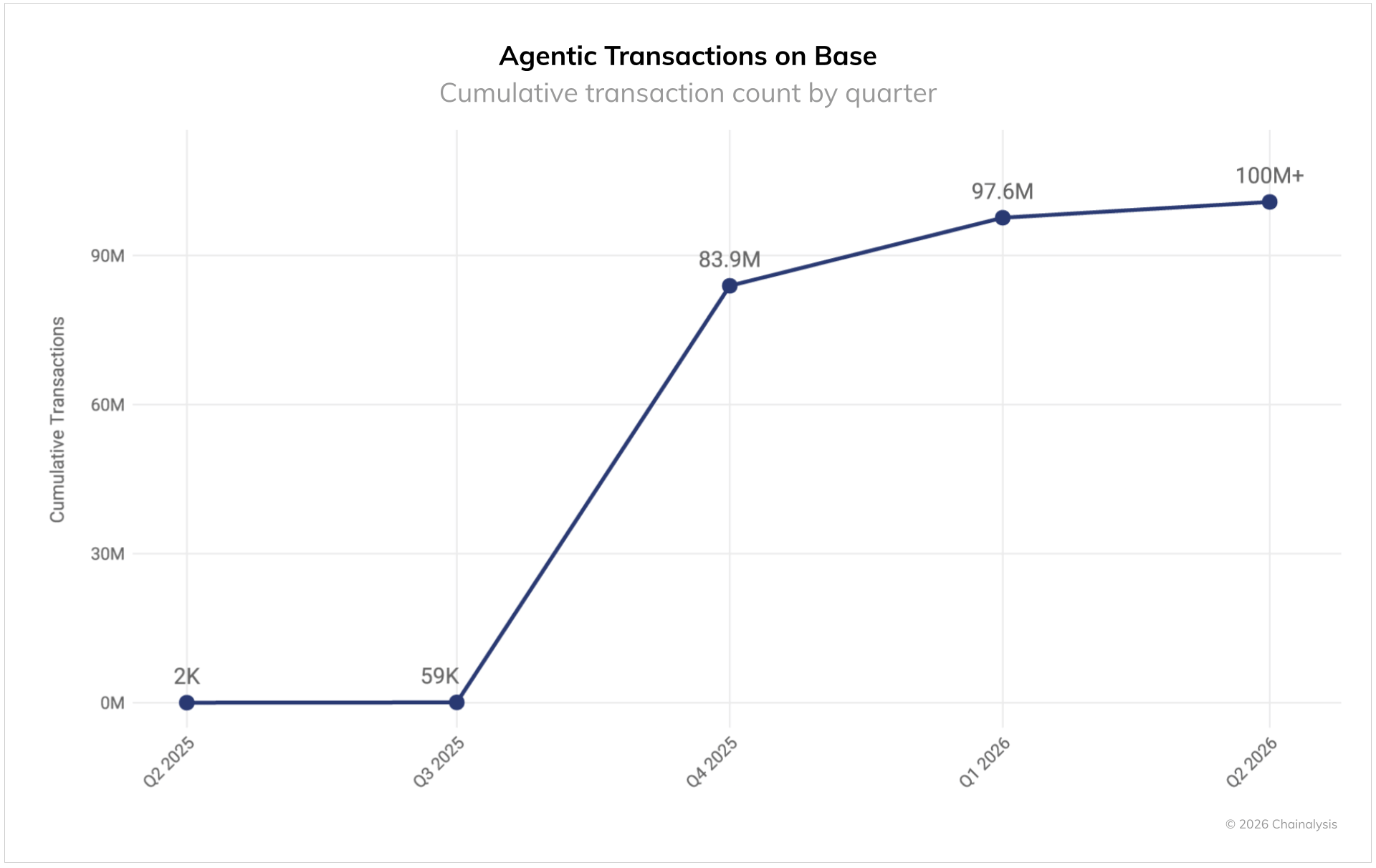

Agentic payment activity on Coinbase’s Base network topped 100 million transactions on June 3, signaling that machine-to-machine payments have moved beyond the proof-of-concept.

Cumulative agentic transfer volumes on Base. Source: Chainalysis

The x402 protocol allows software agents to make onchain payments directly through web requests.

Magazine: ‘Accidental jailbreaks’ and ChatGPT’s links to murder, suicide