Few tech innovations have been as transformative as generative artificial intelligence. Since ChatGPT’s launch in November 2022, the AI landscape has evolved dramatically, challenging long-held norms and reshaping entire industries. The source of the latest

shake-up has been DeepSeek, whose sudden emergence heaped pressure on industry leaders like OpenAI, Google, and Meta. The Chinese AI lab’s debut also sent shockwaves through the wider tech sector, triggering a market sell-off that wiped over

$1 trillion from U.S. and European technology stocks in a single day, and saw Nvidia lose

$600 billion in market capitalisation — the steepest one-day decline by that measure for any company in U.S. stock market history.

For credit brokers and the broader financial industry, these developments signal both a challenge and an opportunity. Heightened competition in the AI space is likely to drive down costs and foster more accessible AI solutions, empowering businesses to streamline

processes, enhance risk assessments, and improve customer interactions. However, as AI continues to revolutionise credit broking, staying ahead of these technological advances will be essential to maintaining a competitive edge.

Interest and Investment

Goldman Sachs forecasted in 2023 that annual global investments in AI technology would reach nearly $200 billion by 2025. Recent

data suggests that investor enthusiasm for generative AI is accelerating even faster than anticipated. According to

EY, venture capital investment in gen AI nearly doubled in 2024, reaching $45 billion — up from $24 billion in 2023 and more than five times the $8.7 billion invested in 2022. Meanwhile, financial tracker PitchBook

reports that generative AI companies secured a record-breaking $56 billion in venture capital across 885 deals in 2024.

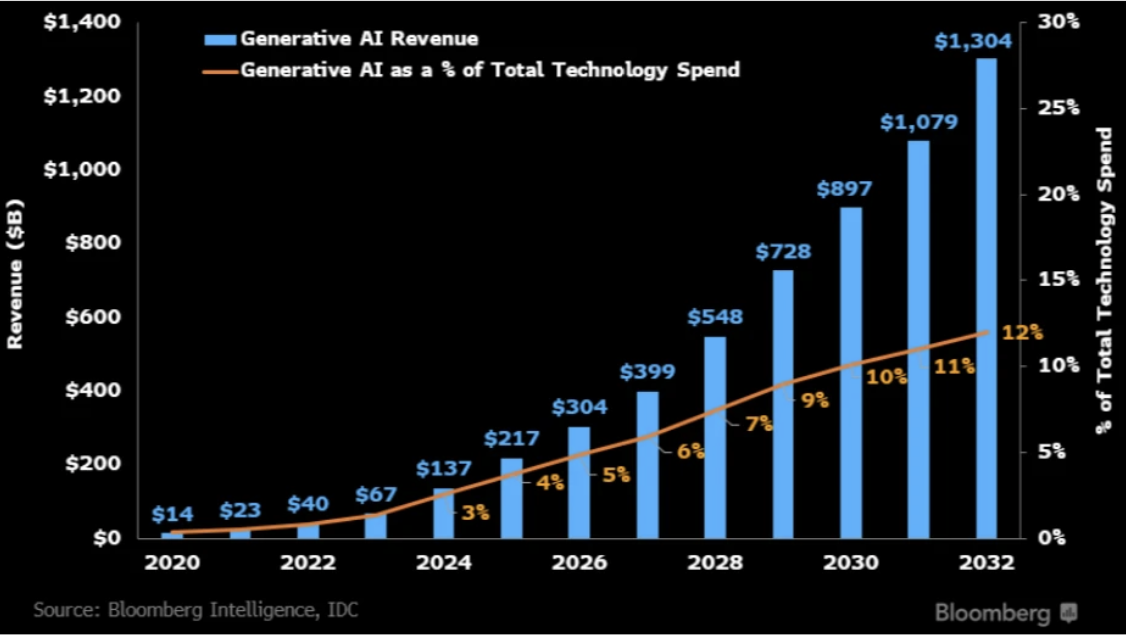

Beyond investment growth, the market itself is projected to expand significantly. Bloomberg Intelligence estimates that the generative

AI sector could grow from $40 billion in 2022 to a staggering $1.3 trillion by 2032, with a compound annual growth rate (CAGR) of 42%.

For the financial sector, particularly credit broking and credit risk management, this AI revolution is already underway. McKinsey’s survey

of senior credit risk executives from 24 financial institutions, including nine of the top ten US banks, found that 20% had already implemented at least one generative AI use case, while another 60% expected to do so within a year. AI-powered tools are being

deployed across the credit life cycle, from hyper-personalised client engagement to automated credit assessments, underwriting, portfolio monitoring, and risk reporting. Portfolio monitoring, in particular, has become a key focus, with nearly 60% of institutions

leveraging AI-driven optimisation strategies to enhance risk management and efficiency.

Use Cases and Their Impacts

Use cases for AI in credit broking are being revised, expanded and built upon all the while but there are a few essential ways in which its impact is already being felt. AI can be deployed, for example, to analyse and summarise unstructured data in ways

that help speed up and enhance specific processes, handily saving businesses both time and money.

Beyond efficiency, AI is transforming client engagement. By leveraging real-time data, AI-driven tools can assess individual financial situations with greater precision, offering hyper-personalised credit products. This is particularly impactful for those

with limited or no credit history, as AI can analyse alternative data — such as on transaction behaviour patterns, utility payments, and mobile usage — to determine creditworthiness. As a result, AI is enabling more inclusive lending, helping individuals and

businesses access financial products that would otherwise be out of reach.

AI is also playing a crucial role in bridging the financial inclusion gap. AI-powered mobile banking and lending platforms are reaching underbanked populations by simplifying account setup, improving financial literacy, and providing tailored credit solutions.

Advanced AI-driven chatbots and voice assistants are making financial services more accessible, particularly for those with limited literacy or technological experience. Additionally, AI-powered risk assessment tools are allowing micro-entrepreneurs and small

businesses to secure funding, boosting economic growth in regions with limited traditional banking infrastructure.

For credit brokers, generative AI can also mean more automation of routine processes. And once credit deals are approved, brokers should be able to streamline the contracting process with the help of AI. The tech can also, potentially at least, help brokers

in putting together all and any written communications they need to send out to their clients, while information about those clients should also become richer and much easier to collect, assess and correlate.

Challenges to Overcome

For anyone involved in credit broking and risk assessment settings, there are clearly some major challenges to overcome as AI becomes an increasingly commonplace part of the picture. Crucially, as use of generative AI is scaled up, credit brokers need to

take seriously a full range of issues associated with governance and risk. Regulators across financial services and worldwide are keeping a close eye on activities and developments around the use of AI, as they are bound to do in keeping with their remit as

protectors of consumer interests and market integrity.

As has always been the case for credit brokers, a fundamental aim must be to avoid any association with notions of unfairness. Standards in that respect will need to be maintained equally, or even improved upon, as generative AI comes into more widespread

use and under the scrutiny of relevant regulators. The danger with letting standards slip in these contexts of course is that businesses might suffer significant reputational damage and trust in their services may wane substantively in ways that hinder their

overall competitiveness.

Transparency too is an important part of the equation for credit brokers making more common use of AI, with consumers and clients sure to expect that high standards of data privacy and security be maintained by any service providers they encounter or engage

with. In simple terms, brokers ought to be able to confidently explain and justify, if ever asked, what they are doing with AI and why, whether they’re responding to questions from clients, prospects, regulators, operating partners, or members of their own

workforce.

Best Laid Plans

Taking a step back and looking at the broader picture around how credit brokers might aim to make best use of AI innovations in the coming years, planning ahead carefully rather than rushing to action could be key. There’s no doubt that major credit risk

players are embracing generative AI, but the challenges and risks involved also represent good reason for some degree of caution to be exercised as necessary.

This somewhat cautious mindset is not limited to credit broking but extends across financial services and beyond. By mid-2024, IT decision-makers were increasingly grappling with the full scope of AI’s implications. While optimism about AI’s impact remains

high, there is a growing focus on strategic planning, robust governance frameworks, data quality, employee upskilling, and scalability.

A compelling example is Moody’s, a leading credit ratings agency, which is modernising commercial lending with its new AI-powered solutions. By automating routine tasks such as loan origination and risk assessment, Moody’s empowers staff to focus on strategic

decisions while uncovering hidden insights through advanced data analysis.

Although AI offers significant potential in automating various processes, the

experiment by Clint Howen’s Hero Broker highlighted that, in areas like mortgage broking, human interaction remains indispensable. Findings from the study revealed that 89.4% of borrowers preferred to speak to a real person before proceeding with their

application, and only 1.4% completed the entire process online without any human help. In contrast to smaller financial products such as credit cards, which can be more easily managed through automated processes, home loans carry emotional weight that technology

alone cannot manage. This emotional aspect of home ownership and borrowing makes the need for human support in such transactions critical.

Ultimately, while AI is clearly poised to revolutionise many areas of the financial industry, a balanced approach, combining automation with human oversight, is key for the future of credit broking. AI enhances efficiency, but human expertise remains essential

for managing the complexities of financial decisions. Credit brokers who blend both will be best positioned to succeed in the evolving financial landscape.

Opportunities for Transformation

Looking ahead, generative AI clearly has huge potential to transform credit industries worldwide, to boost financial inclusion, and to connect borrowers with lenders more seamlessly and efficiently than ever before. That potential is already compelling and,

in years to come, AI will no doubt be used not just to address pain points or speed up specific processes, but throughout the credit broking life cycle in ways that are eventually taken completely for granted.

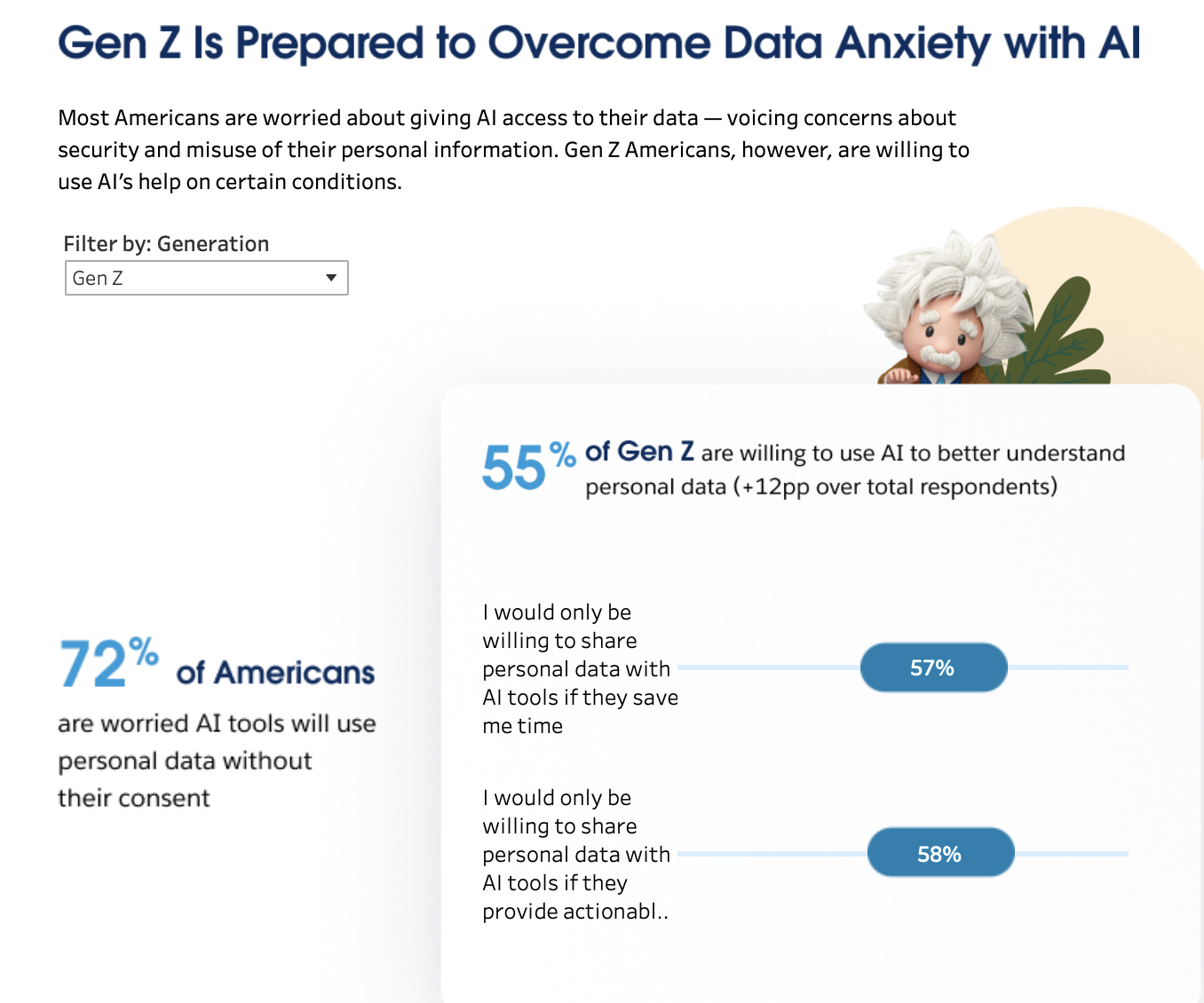

Salesforce figures showed recently that younger cohorts of consumers, particularly those within the ‘Gen Z’ generation, are most ready for and happy to encounter gen AI services

and solutions to better understand what to do with their data. Those findings tie in neatly with the notion that AI technology will inevitably become much more commonplace and widely relied upon in years to come in data-driven contexts like credit broking.

Source: https://www.salesforce.com/uk/news/stories/gen-z-data-trends/

For brokers themselves, there are risks to be considered carefully, as there are with any emerging and potentially game-changing technologies. The key to success may well be embracing the challenges that the AI revolution brings, while also trusting that

demand for human expertise and experience that consistently makes a positive difference will always be in high demand.